Energy powers society; society's choices shape energy policy. A blog about our energy resources and the choices they present for society.

Showing posts with label Henry Hub. Show all posts

Showing posts with label Henry Hub. Show all posts

FERC 2014 State of the Markets report

Monday, March 23, 2015

U.S. energy markets overseen by the Federal Energy Regulatory Commission in 2014 were impacted by extreme weather and changes in the mix of electric generation resources, according to a report by Commission staff.

The 2014 State of the Markets report issued on March 19 by FERC's Office of Enforcement’s Division of Energy Market Oversight presents Commission's staff’s assessment of recent developments in natural gas, electric, and other energy markets.

Extreme cold temperatures in the first quarter of 2014 affected natural gas infrastructure and power markets across the country. The price of natural gas in the U.S. reached record high levels, driving corresponding spikes in the price of electricity. For example, the price of natural gas at the Transco Zone 6 Non-NY pricing point hit $123/MMBtu in January -- about 33 times higher than the average 2013 U.S. price. Largely due to these price spikes, the spot natural gas price at the Henry Hub pricing point averaged $4.32/MMBtu in 2014, a 16% increase over 2013.

Meanwhile, natural gas and renewable resources continued to displace coal as a fuel for electric power generation. Total U.S. generating capacity increased 10.8 GW in 2014, with natural gas and renewable projects representing the bulk of new capacity. At the same time, utilities retired coal-fired power plants, continuing a trend that started in 2012. Commission staff projects continued coal retirements in 2015, particularly after the April effective date of additional air emissions regulations imposed by the Environmental Protection Agency's Mercury and Air Toxics Standards.

FERC's 2014 State of the Markets report also provides a quick look at 2015 year-to-date market performance. Wholesale electricity prices rose again this winter, although not as sharply as in the first quarter of 2014. FERC staff's report suggests factors helping to moderate winter prices included better cold-weather preparation of assets, programs like ISO New England's Winter Reliability Program, better coordination between operators of electric transmission and natural gas pipelines, record high levels of natural gas production, the development of new pipeline infrastructure, and low oil prices.

Federal report details U.S. natural gas market

Monday, May 20, 2013

Last week the Federal Energy Regulatory Commission's Office of Enforcement released its assessment of domestic natural gas, electric and other energy markets. The 2012 State of the Markets report (14-page PDF) describes how changes in both supply and demand led to record low pricing for natural gas at the same time as record high demand for that fuel.

2012 saw significant increases in the production of natural gas from shale and other unconventional resources. Domestic natural gas production grew 5 percent, reaching a new all-time record. Improved drilling rig efficiency boosted production from the Marcellus shale in Pennsylvania, Texas’s Eagle Ford shale, and the Fayetteville shale in Arkansas. Shale gas production rose from 22 percent of total U.S. natural gas production in 2011 to 38 percent by the end of 2012.

At the same time, total average daily natural gas demand reached a new record, growing 4 percent to 70 Bcf/d in 2012. This growth in demand occurred despite a 10 percent drop in residential and commercial demand for natural gas due to the warm winter. Growth in demand for natural gas for electric power generation surged, driven by the low price of gas and tougher environmental regulations on coal-fired power plants. Generators’ demand for natural gas grew 21 percent over 2011, reaching a record 25 Bcf/d and surpassing residential and commercial demand for the first time in history. Natural gas replaced coal in many places; coal-fired generation fell to the lowest level in 30 years. Since natural gas is often the marginal fuel in electric generation, lower natural gas prices generally resulted in lower electric prices across the country.

The combination of these changes in supply and demand led U.S. natural gas prices to a ten-year low last year. The spot price at the Henry Hub trading point averaged $2.74/MMBtu for the year, down 31 percent from 2011. Spot prices at Henry Hub ranged from a low of $1.82/MMBtu to $3.77/MMBtu at the onset of the winter heating season. Most of the country enjoyed low natural gas prices, although pipeline constraints led to much higher pricing in New England, particularly in the winter.

2012 saw significant increases in the production of natural gas from shale and other unconventional resources. Domestic natural gas production grew 5 percent, reaching a new all-time record. Improved drilling rig efficiency boosted production from the Marcellus shale in Pennsylvania, Texas’s Eagle Ford shale, and the Fayetteville shale in Arkansas. Shale gas production rose from 22 percent of total U.S. natural gas production in 2011 to 38 percent by the end of 2012.

At the same time, total average daily natural gas demand reached a new record, growing 4 percent to 70 Bcf/d in 2012. This growth in demand occurred despite a 10 percent drop in residential and commercial demand for natural gas due to the warm winter. Growth in demand for natural gas for electric power generation surged, driven by the low price of gas and tougher environmental regulations on coal-fired power plants. Generators’ demand for natural gas grew 21 percent over 2011, reaching a record 25 Bcf/d and surpassing residential and commercial demand for the first time in history. Natural gas replaced coal in many places; coal-fired generation fell to the lowest level in 30 years. Since natural gas is often the marginal fuel in electric generation, lower natural gas prices generally resulted in lower electric prices across the country.

The combination of these changes in supply and demand led U.S. natural gas prices to a ten-year low last year. The spot price at the Henry Hub trading point averaged $2.74/MMBtu for the year, down 31 percent from 2011. Spot prices at Henry Hub ranged from a low of $1.82/MMBtu to $3.77/MMBtu at the onset of the winter heating season. Most of the country enjoyed low natural gas prices, although pipeline constraints led to much higher pricing in New England, particularly in the winter.

2012 natural gas wholesale prices fell 31%

Monday, January 14, 2013

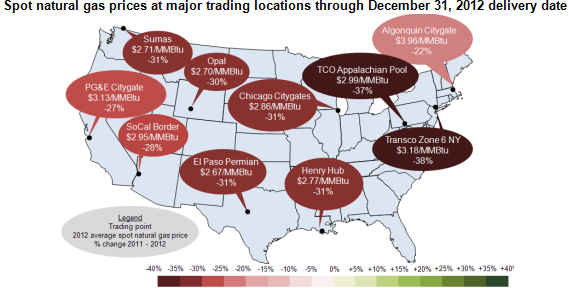

2012's biggest revolution in the energy sector may be the commercial availability of low-cost natural gas. Significant growth in the volume of shale gas produced by hydraulic fracturing, combined with mild demand for natural gas, resulted in 2012 average wholesale prices that were 31% below 2011 prices.

As a commodity, prices for natural gas are typically stated at a pricing point known as Henry Hub, a pipeline distribution hub in Erath, Louisiana. In 2011, the average price at Henry Hub was $4.02 per million British thermal units (MMBtu). In 2012, that price fell to $2.77 per MMBtu, the lowest average annual price at Henry Hub since 1999.

Overall, average annual prices for natural gas fell 30%-34% in 2012 compared to 2011 for buyers at most major trading points. The U.S. Energy Information Administration recently released this chart showing average spot prices for natural gas in 2012, and the percent change since 2011:

The historic low pricing is driven by several factors. Natural gas production was up 4% compared to 2011 levels, particularly from the Marcellus Shale and Eagle Ford basins. Gas inventories in storage remained high. At the same time, demand rose by 3%; increased use of natural gas for electric power generation was partially offset by a relatively mild winter.

What will 2013 hold for natural gas pricing?

Marcellus shale gas drilling slows

Tuesday, July 10, 2012

Natural gas drilling activity has declined in parts of the Marcellus Shale formation under Pennsylvania and other eastern states, largely as a result of low gas prices. These prices in turn are largely the result of significant increases in the available supply of recoverable natural gas made possible by horizontal drilling techniques and hydraulic fracturing or fracking. As a consequence, many natural gas producers are focusing on areas of shale rich in both gas and natural gas liquids.

The Marcellus Shale, a layer of ancient marine sediment rich in organic material and extending beneath Pennsylvania, Ohio, West Virginia, New York, and Maryland, is believed to be one of the world's largest natural gas fields. In 2008, drilling activity in the Marcellus Shale began to increase significantly, as these newer drilling techniques and increases in the price of other fuels like oil made the shale gas economically feasible to recover. (Compare this map of Marcellus shale drilling activity in Pennsylvania from 7/25/2008 to this map of permits issued as of March 9, 2012.) As of this spring, Pennsylvania alone had issued 11,772 permits for vertical and horizontal gas wells in the Marcellus formation.

One result of the expansion of shale gas production is a significant decrease in the price of natural gas. Since 2008, natural gas prices at the Henry Hub in Louisiana (where gas as a commodity is typically priced) have fallen from over $12 per million British thermal units (MMBtu) to as low as $2 per MMBtu. Other factors have played a role in this price decline, such as a mild winter with lower-than-expected heating demand and the overall economic slowdown, but the increase in supply due to shale gas production is viewed as a major cause of the price decline.

Now, one of the effects of the price decline is a decrease in natural gas drilling activity. This decrease is particularly marked in areas where the shale produces "dry gas", or natural gas that is primarily methane and is low in so-called natural gas liquids. Natural gas liquids -- hydrocarbons other than methane that are extracted when natural gas is processed in a natural gas treatment facility -- include ethane, propane, and butanes. These natural gas liquids are important feedstocks for the production of many chemicals and plastics, and add value to the natural gas produced from "wet" shales.

Where shale gas contains significant amounts of natural gas liquids, production appears steady or increasing, while gas producers in areas with lower amounts of natural gas liquids are now saying that they are having a hard time making money off gas alone. If this trend continues, areas of dry gas like much of the known portions of the Marcellus Shale may continue to see a slowdown in drilling activity while producers focus on areas rich in natural gas liquids.

The Marcellus Shale, a layer of ancient marine sediment rich in organic material and extending beneath Pennsylvania, Ohio, West Virginia, New York, and Maryland, is believed to be one of the world's largest natural gas fields. In 2008, drilling activity in the Marcellus Shale began to increase significantly, as these newer drilling techniques and increases in the price of other fuels like oil made the shale gas economically feasible to recover. (Compare this map of Marcellus shale drilling activity in Pennsylvania from 7/25/2008 to this map of permits issued as of March 9, 2012.) As of this spring, Pennsylvania alone had issued 11,772 permits for vertical and horizontal gas wells in the Marcellus formation.

One result of the expansion of shale gas production is a significant decrease in the price of natural gas. Since 2008, natural gas prices at the Henry Hub in Louisiana (where gas as a commodity is typically priced) have fallen from over $12 per million British thermal units (MMBtu) to as low as $2 per MMBtu. Other factors have played a role in this price decline, such as a mild winter with lower-than-expected heating demand and the overall economic slowdown, but the increase in supply due to shale gas production is viewed as a major cause of the price decline.

Now, one of the effects of the price decline is a decrease in natural gas drilling activity. This decrease is particularly marked in areas where the shale produces "dry gas", or natural gas that is primarily methane and is low in so-called natural gas liquids. Natural gas liquids -- hydrocarbons other than methane that are extracted when natural gas is processed in a natural gas treatment facility -- include ethane, propane, and butanes. These natural gas liquids are important feedstocks for the production of many chemicals and plastics, and add value to the natural gas produced from "wet" shales.

Where shale gas contains significant amounts of natural gas liquids, production appears steady or increasing, while gas producers in areas with lower amounts of natural gas liquids are now saying that they are having a hard time making money off gas alone. If this trend continues, areas of dry gas like much of the known portions of the Marcellus Shale may continue to see a slowdown in drilling activity while producers focus on areas rich in natural gas liquids.

Subscribe to:

Posts (Atom)