Virginia’s largest electric utility is launching a feed-in

tariff for solar energy – but will it work?

Feed-in

tariffs are a policy tool used to facilitate the production of renewable electricity. While six states and a handful of utilities have

each designed their own programs, in general feed-in tariffs guarantee that

customers who own solar panels or eligible renewable electricity generation

projects a fixed price to sell the power to their local utility. Building solar photovoltaic and other

renewable generation technologies can have a relatively high capital cost, but the

lack of a fuel cost can lead to low operational costs in the long run. Customers, particularly businesses, say they need

certainty about the internal economics of their project – whether revenue

streams or savings off existing power bills – prior to committing the capital

to actually build it. Feed-in tariffs are

one tool to address this uncertainty.

Dominion Virginia

Power serves ratepayers in the Commonwealth as Virginia Electric and Power

Co. It is a subsidiary of Dominion

Resources Inc. After securing an

approval from the Virginia State Corporation Commission last March, the

utility recently proposed a pilot feed-in tariff program for solar resources. Under the Solar Purchase Program, Dominion

will provide five-year contracts to purchase the energy produced by eligible rooftop

solar projects and other distributed solar photovoltaic resources.

The program guarantees a price of 15 cents per kilowatt-hour

over the contracts’ term. This price paid to solar

energy producers is above Dominion’s recent retail average electricity price. In 2012, Virginia's average retail

electricity price was 10.5 cents per kWh for residential customers. Commercial customers paid an average price of

just 7.8 cents per kWh; the increased spread between the feed-in tariff rate for

sales to the utility and commercial customers’ average price for purchases from

it creates a strong incentive for commercial customers to develop solar

projects.

Despite significant interest in Virginia and elsewhere in the

development of the feed-in tariff, Dominion’s program is only a pilot project. It applies only to residential systems up to

20 kilowatts and commercial systems up to 50 kW in size. Moreover, the feed-in tariff is capped at 3

MW in total participating capacity.

Coupled with solar projects’ capacity factors, this limits the total

volume of electricity to be purchased under the program.

Will Dominion’s feed-in tariff work? The answer depends on what “working”

means. If the price spread between the

feed-in tariff rates and retail rates, combined with other incentives such as

federal tax credits, the feed-in tariff may be enough to encourage the

development of some commercial and residential systems. The utility and ratepayers may learn more

about the costs and benefits of distributed generation. To some degree, it may incentivize activity and

competition in the solar installation business.

But where the program is capped at 3 MW, the current feed-in

tariff program alone may neither spur much new investment nor cost ratepayers

much. Dominion’s recent peak loads were

about 19,636 MW – so solar purchases would represent just hundredths of a

percent by capacity, and an even smaller number by volume of electricity sold. The entire program cap could be taken up by 60

commercial-scale projects, or even by 750 homes using Dominion’s estimated

average of 4 kW per residential project.

It is unclear if this level of volume is enough to lead to a more robust

installation services sector, or to lower costs for installed solar projects.

Implementation of Dominion’s solar feed-in tariff program

will follow State Corporation Commission review and approval.

Energy powers society; society's choices shape energy policy. A blog about our energy resources and the choices they present for society.

Coal retakes the lead in US electric power generation

Friday, May 24, 2013

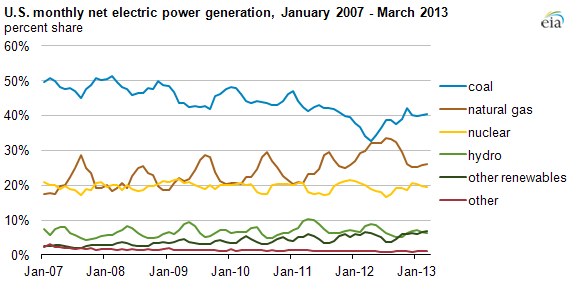

Coal has retaken its status as the leading fuel for electric power generation in the U.S., as both demand for electricity and natural gas prices increased. Preliminary U.S. Energy Information Administration data show that 40% or more of the nation's

electricity came from coal in each month between November 2012 and March 2013, with natural gas fueling

about 25% of generation during the same period. This is a partial reversal of the recent trend of natural gas replacing coal as a fuel for electric power generation.

Coal dominated electric power production for much of last century. From 2001 to 2008, coal powered between 48% and 51% of annual generation. But in the past four years, increased production of natural gas from shales and other unconventional resources led to lower natural gas prices. Combined with tighter environmental regulations on coal plants' air emissions, this led utilities and merchant generators to burn more natural gas and less coal. By April 2012, coal and natural gas each contributed an equal share of electric power.

EIA's most recent data suggests that trend is slowing or has partially reversed. For the five months from November 2012 through March 2013, more electricity was produced in the U.S. from coal than from natural gas. For example, in March, coal-fired units generated just 130,000 megawatt-hours of electricity, while natural gas units produced just under 85,000 megawatt-hours.

Coal's share of total U.S. electricity generation remains well below its historic range. Coal has not been responsible for 50% or more of power produced in any year since 2005, and the EIA's latest Short-Term Energy Outlook predicts that coal will contribute 40% of generation in 2013. Natural gas remains relatively inexpensive throughout most of the year in most of the country, but regions like New England suffer from higher natural gas prices in winter due to inadequate pipeline infrastructure into the region. Market forces and regulations will determine whether natural gas climbs back to parity with coal as a fuel for electric power generation.

Coal dominated electric power production for much of last century. From 2001 to 2008, coal powered between 48% and 51% of annual generation. But in the past four years, increased production of natural gas from shales and other unconventional resources led to lower natural gas prices. Combined with tighter environmental regulations on coal plants' air emissions, this led utilities and merchant generators to burn more natural gas and less coal. By April 2012, coal and natural gas each contributed an equal share of electric power.

EIA's most recent data suggests that trend is slowing or has partially reversed. For the five months from November 2012 through March 2013, more electricity was produced in the U.S. from coal than from natural gas. For example, in March, coal-fired units generated just 130,000 megawatt-hours of electricity, while natural gas units produced just under 85,000 megawatt-hours.

|

| Chart courtesy of U.S. Energy Information Administration, available at http://www.eia.gov/todayinenergy/detail.cfm?id=11391/ |

Coal's share of total U.S. electricity generation remains well below its historic range. Coal has not been responsible for 50% or more of power produced in any year since 2005, and the EIA's latest Short-Term Energy Outlook predicts that coal will contribute 40% of generation in 2013. Natural gas remains relatively inexpensive throughout most of the year in most of the country, but regions like New England suffer from higher natural gas prices in winter due to inadequate pipeline infrastructure into the region. Market forces and regulations will determine whether natural gas climbs back to parity with coal as a fuel for electric power generation.

Federal report details U.S. natural gas market

Monday, May 20, 2013

Last week the Federal Energy Regulatory Commission's Office of Enforcement released its assessment of domestic natural gas, electric and other energy markets. The 2012 State of the Markets report (14-page PDF) describes how changes in both supply and demand led to record low pricing for natural gas at the same time as record high demand for that fuel.

2012 saw significant increases in the production of natural gas from shale and other unconventional resources. Domestic natural gas production grew 5 percent, reaching a new all-time record. Improved drilling rig efficiency boosted production from the Marcellus shale in Pennsylvania, Texas’s Eagle Ford shale, and the Fayetteville shale in Arkansas. Shale gas production rose from 22 percent of total U.S. natural gas production in 2011 to 38 percent by the end of 2012.

At the same time, total average daily natural gas demand reached a new record, growing 4 percent to 70 Bcf/d in 2012. This growth in demand occurred despite a 10 percent drop in residential and commercial demand for natural gas due to the warm winter. Growth in demand for natural gas for electric power generation surged, driven by the low price of gas and tougher environmental regulations on coal-fired power plants. Generators’ demand for natural gas grew 21 percent over 2011, reaching a record 25 Bcf/d and surpassing residential and commercial demand for the first time in history. Natural gas replaced coal in many places; coal-fired generation fell to the lowest level in 30 years. Since natural gas is often the marginal fuel in electric generation, lower natural gas prices generally resulted in lower electric prices across the country.

The combination of these changes in supply and demand led U.S. natural gas prices to a ten-year low last year. The spot price at the Henry Hub trading point averaged $2.74/MMBtu for the year, down 31 percent from 2011. Spot prices at Henry Hub ranged from a low of $1.82/MMBtu to $3.77/MMBtu at the onset of the winter heating season. Most of the country enjoyed low natural gas prices, although pipeline constraints led to much higher pricing in New England, particularly in the winter.

2012 saw significant increases in the production of natural gas from shale and other unconventional resources. Domestic natural gas production grew 5 percent, reaching a new all-time record. Improved drilling rig efficiency boosted production from the Marcellus shale in Pennsylvania, Texas’s Eagle Ford shale, and the Fayetteville shale in Arkansas. Shale gas production rose from 22 percent of total U.S. natural gas production in 2011 to 38 percent by the end of 2012.

At the same time, total average daily natural gas demand reached a new record, growing 4 percent to 70 Bcf/d in 2012. This growth in demand occurred despite a 10 percent drop in residential and commercial demand for natural gas due to the warm winter. Growth in demand for natural gas for electric power generation surged, driven by the low price of gas and tougher environmental regulations on coal-fired power plants. Generators’ demand for natural gas grew 21 percent over 2011, reaching a record 25 Bcf/d and surpassing residential and commercial demand for the first time in history. Natural gas replaced coal in many places; coal-fired generation fell to the lowest level in 30 years. Since natural gas is often the marginal fuel in electric generation, lower natural gas prices generally resulted in lower electric prices across the country.

The combination of these changes in supply and demand led U.S. natural gas prices to a ten-year low last year. The spot price at the Henry Hub trading point averaged $2.74/MMBtu for the year, down 31 percent from 2011. Spot prices at Henry Hub ranged from a low of $1.82/MMBtu to $3.77/MMBtu at the onset of the winter heating season. Most of the country enjoyed low natural gas prices, although pipeline constraints led to much higher pricing in New England, particularly in the winter.

Oregon coal export plans stopped

Thursday, May 9, 2013

The United

States is one of the world’s top coal producers and exporters, but recent plans

to add coal export capacity in the Pacific Northwest have not been fulfilled,

as several proposed export terminals have been withdrawn. Plans for yet another terminal have been

scrapped, as yesterday Kinder Morgan Energy Partners LP canceled its proposed

Clatskanie, Oregon project. What does

this mean for U.S. coal exports and for domestic pricing?

Kinder Morgan Energy Partners is a publicly traded master-limited partnership,or MLP, focused on pipeline infrastructure. Along with fellow Kinder Morgan family companies Kinder Morgan, Inc., Kinder Morgan Management, LLC, and El Paso Pipeline Partners, Kinder Morgan claims to be the largest midstream and the third largest energy company (based on combined enterprise value) in North America. The company owns or operates about 80,000 miles of pipelines and 180 terminals handling products like natural gas, refined petroleum products, crude oil, and carbon dioxide, as well as gasoline, jet fuel, ethanol, coal, petroleum coke and steel. It boasts of operating primarily “like a giant toll road”, and seeks to avoid commodity price risk through a fee-for-service model.

Most coal export capacity in the U.S. is located in the Midatlantic and Gulf Coast regions. While Asia dominates the world coal import market, major markets for U.S. coal exports include Canada, Brazil, the Netherlands, and the European Union. The principal West Coast coal export port is Los Angeles/Long Beach, with virtually no export capacity in the Pacific Northwest. Kinder Morgan had proposed a terminal to be built at the Port Westward industrial park on the Columbia River near Clatskanie. Yesterday project partner Port of St. Helens stated that Kinder Morgan had announced that it would not be pursuing the project.

Up to six Pacific Northwest coal export terminates have been proposed in recent years, but to date none have been built. The Kinder Morgan proposal joins a series of other canceled Pacific Northwest coal export plans. RailAmerica Inc. announced last year that it would not pursue a coal storage and export facility at Washington’s Port of Grays Harbor. Earlier this year, the Oregon International Port of Coos Bay announced the end of its exclusive negotiating agreement between with Metropolitan Stevedoring Company (Metro Ports) to build a thermal coal and biomass export facility. With the Kinder Morgan project gone, three potential terminals remain: Australian company Ambre Energy’s barge-loading operation at the port of Morrow and Port Westward, Millennium Bulk Terminals’ proposed $643 million dock west of Longview, and SSA Marine’s proposed $600 million coal terminal at Cherry Point.

Kinder Morgan Energy Partners is a publicly traded master-limited partnership,or MLP, focused on pipeline infrastructure. Along with fellow Kinder Morgan family companies Kinder Morgan, Inc., Kinder Morgan Management, LLC, and El Paso Pipeline Partners, Kinder Morgan claims to be the largest midstream and the third largest energy company (based on combined enterprise value) in North America. The company owns or operates about 80,000 miles of pipelines and 180 terminals handling products like natural gas, refined petroleum products, crude oil, and carbon dioxide, as well as gasoline, jet fuel, ethanol, coal, petroleum coke and steel. It boasts of operating primarily “like a giant toll road”, and seeks to avoid commodity price risk through a fee-for-service model.

Most coal export capacity in the U.S. is located in the Midatlantic and Gulf Coast regions. While Asia dominates the world coal import market, major markets for U.S. coal exports include Canada, Brazil, the Netherlands, and the European Union. The principal West Coast coal export port is Los Angeles/Long Beach, with virtually no export capacity in the Pacific Northwest. Kinder Morgan had proposed a terminal to be built at the Port Westward industrial park on the Columbia River near Clatskanie. Yesterday project partner Port of St. Helens stated that Kinder Morgan had announced that it would not be pursuing the project.

Up to six Pacific Northwest coal export terminates have been proposed in recent years, but to date none have been built. The Kinder Morgan proposal joins a series of other canceled Pacific Northwest coal export plans. RailAmerica Inc. announced last year that it would not pursue a coal storage and export facility at Washington’s Port of Grays Harbor. Earlier this year, the Oregon International Port of Coos Bay announced the end of its exclusive negotiating agreement between with Metropolitan Stevedoring Company (Metro Ports) to build a thermal coal and biomass export facility. With the Kinder Morgan project gone, three potential terminals remain: Australian company Ambre Energy’s barge-loading operation at the port of Morrow and Port Westward, Millennium Bulk Terminals’ proposed $643 million dock west of Longview, and SSA Marine’s proposed $600 million coal terminal at Cherry Point.

Whether a coal export terminal will be developed in the Pacific

Northwest is uncertain. If not, it will

continue to be difficult for coal produced in the western U.S. to reach the

world’s largest demands for coal imports.

China, Japan,

South Korea, India, and even the relatively small Chinese Taipei have led the demand

for coal imports in recent years. This opens significant economic activity. At the

same time, environmentalists argue that new export projects would contribute to

global pollution and greenhouse gas emissions.

Combined with the pressures of the commodity market for coal and other

fuels, these dynamics may continue to block expanded West Coast export plans. As is being argued over the issue of

liquefied natural gas exports, whether coal exports are expanded could also

have impacts for U.S. coal pricing.

Massachusetts solar power goal reached, expanded

Wednesday, May 8, 2013

Massachusetts has surpassed its goal of being home to 250 megawatts of installed solar energy capacity four years early. Governor Deval Patrick's administration and the state legislature have adopted a series of policies favoring the development of solar energy, including a target of reaching 250 MW by 2017. Last week the administration announced that this goal had already been reached, and established a new goal of 1,600 MW by 2020.

Solar power in Massachusetts has grown significantly in recent years. In 2007, the Commonwealth hosted just 3 MW of solar capacity. Since then, Massachusetts has adopted a variety of incentives for renewable power production. Chief among these is the Renewable Portfolio Standard (RPS) Solar Carve-Out program. State law currently requires utilities to source up to 400 MW from in-state solar photovoltaic projects. Utilities purchase solar renewable energy certificates, or SRECs, representing the environmental attributes of electricity produced by qualified projects. These SRECs come in addition to the actual power produced by projects, and carry a premium value over other renewable attribute products. State laws such as the 2008 Green Communities Act have provided additional incentives, including technical assistance and financial support for solar development.

Given current policies and market dynamics, solar power in Massachusetts will likely continue to grow. While the bulk of newly installed capacity is likely to be in the form of distributed generation (as opposed to very large-scale utility installations as are under development in the desert Southwest), Massachusetts will continue to see projects ranging from residential rooftop-scale to close to 10 MW. Reaching 1,600 MW within the next seven years will be a challenge, and may depend on continued policy support and market trends, but the recent rate of growth and relative enthusiasm suggest this may be possible.

Solar power in Massachusetts has grown significantly in recent years. In 2007, the Commonwealth hosted just 3 MW of solar capacity. Since then, Massachusetts has adopted a variety of incentives for renewable power production. Chief among these is the Renewable Portfolio Standard (RPS) Solar Carve-Out program. State law currently requires utilities to source up to 400 MW from in-state solar photovoltaic projects. Utilities purchase solar renewable energy certificates, or SRECs, representing the environmental attributes of electricity produced by qualified projects. These SRECs come in addition to the actual power produced by projects, and carry a premium value over other renewable attribute products. State laws such as the 2008 Green Communities Act have provided additional incentives, including technical assistance and financial support for solar development.

Given current policies and market dynamics, solar power in Massachusetts will likely continue to grow. While the bulk of newly installed capacity is likely to be in the form of distributed generation (as opposed to very large-scale utility installations as are under development in the desert Southwest), Massachusetts will continue to see projects ranging from residential rooftop-scale to close to 10 MW. Reaching 1,600 MW within the next seven years will be a challenge, and may depend on continued policy support and market trends, but the recent rate of growth and relative enthusiasm suggest this may be possible.

Grid operator expects sufficient electricity this summer

Wednesday, May 1, 2013

Regional electricity grid operator ISO New England, Inc. issued its 2013 summer outlook on April 29. In that report, New England regional transmission organization found that regional electricity supplies during the upcoming summer are expected to be sufficient to meet consumer demand under normal weather conditions. But if any number of contingencies occur, such as a heat wave, the grid could be seriously strained.

ISO New England noted that under normal conditions, there should be enough electricity this summer. But it identified a series of risk factors could tip the balance of supply and demand for electricity, including extreme summer weather conditions or unexpected resource outages. These factors could create "operational challenges", meaning a hard time finding enough electricity to meet peak demand. New England may be forced to resort to importing emergency power from neighboring regions, and asking businesses and people to voluntarily conserve energy.

The report's base assumption is for "normal" summer weather conditions of about 90 degrees in key southern New England cities. Under these conditions, ISO New England forecasts electricity demand could reach 26,690 megawatts (MW). If an extended heat wave pushes temperatures to 95, demand could rise to 28,985 MW. Last summer’s load peaked July 17 at 25,880 MW, about 3% smaller than the base amount forecast for summer 2013. New England set its record for peak demand on August 2, 2006, when demand reached 28,130 MW.

On the supply side, ISO New England identified several risks that could lead to unexpected shortages of electricity. First, most natural gas pipeline maintenance in the region is scheduled for the summer months. Maintenance activities could affect natural gas supplies to some power plants. On this point, the grid operator said it was coordinating with the pipeline companies to ensure that the supply is adequate for power generation during the maintenance season.

Second, liquefied natural gas (LNG) is in high global demand. Current LNG prices are roughly three times higher in Europe and Japan than in the United States. This mean LNG deliveries into New England might be reduced this summer. At times, New England electric generation relies on LNG, which could also affect power plant operations.

Overall, ISO New England reported that it expects electricity supplies to be sufficient to meet consumer demand under normal weather conditions this summer. If shortages occur, they will likely affect both the reliability of the grid and the wholesale price of power. The winter season is likely to be worse, as regional demand for natural gas for heating increases during the winter, placing a tighter squeeze on the amount and price of gas available for electric generation. The grid operator's prediction will be put to the test in the coming months.

ISO New England noted that under normal conditions, there should be enough electricity this summer. But it identified a series of risk factors could tip the balance of supply and demand for electricity, including extreme summer weather conditions or unexpected resource outages. These factors could create "operational challenges", meaning a hard time finding enough electricity to meet peak demand. New England may be forced to resort to importing emergency power from neighboring regions, and asking businesses and people to voluntarily conserve energy.

The report's base assumption is for "normal" summer weather conditions of about 90 degrees in key southern New England cities. Under these conditions, ISO New England forecasts electricity demand could reach 26,690 megawatts (MW). If an extended heat wave pushes temperatures to 95, demand could rise to 28,985 MW. Last summer’s load peaked July 17 at 25,880 MW, about 3% smaller than the base amount forecast for summer 2013. New England set its record for peak demand on August 2, 2006, when demand reached 28,130 MW.

On the supply side, ISO New England identified several risks that could lead to unexpected shortages of electricity. First, most natural gas pipeline maintenance in the region is scheduled for the summer months. Maintenance activities could affect natural gas supplies to some power plants. On this point, the grid operator said it was coordinating with the pipeline companies to ensure that the supply is adequate for power generation during the maintenance season.

Second, liquefied natural gas (LNG) is in high global demand. Current LNG prices are roughly three times higher in Europe and Japan than in the United States. This mean LNG deliveries into New England might be reduced this summer. At times, New England electric generation relies on LNG, which could also affect power plant operations.

Overall, ISO New England reported that it expects electricity supplies to be sufficient to meet consumer demand under normal weather conditions this summer. If shortages occur, they will likely affect both the reliability of the grid and the wholesale price of power. The winter season is likely to be worse, as regional demand for natural gas for heating increases during the winter, placing a tighter squeeze on the amount and price of gas available for electric generation. The grid operator's prediction will be put to the test in the coming months.

Subscribe to:

Posts (Atom)